Econometrics Toolbox 提供用于时间序列数据分析和建模的函数与交互式工作流。该工具箱提供多种用于模型选择的可视化和诊断,包括针对自相关和异方差性、单位根和平稳性、协整性、因果性以及结构性更改的测试。您可以使用各种建模框架来估计、仿真和预测经济系统。这些框架既可以通过计量经济学建模器以交互方式使用,也可以通过工具箱中提供的函数以编程方式使用。这些框架包括回归、ARIMA、状态空间、GARCH、多元 VAR 和多元 VEC、以及转变模型。该工具箱还提供了贝叶斯工具,用于开发可基于新数据进行学习的时变模型。

条件均值和回归建模

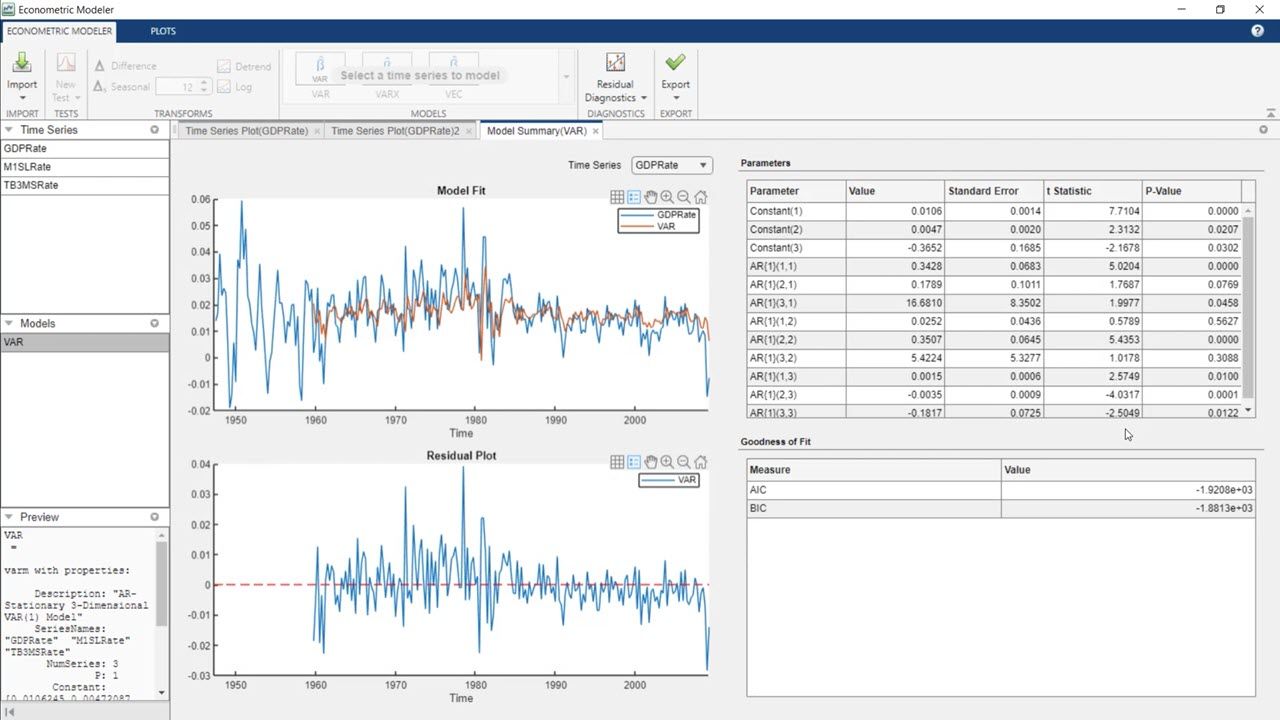

使用 ARIMA、贝叶斯回归、向量自回归 (VAR) 和向量误差修正 (VEC) 等模型对一元和多元时间序列进行拟合、仿真和预测。

的因子分布")

产品资源:

“我的专长是金融,而不是编程。为了对海量数据进行复杂分析,我需要一款易于使用且包括许多所需函数的软件。有了 MATLAB,我能在同一个环境中完成所有工作,这确实非常有用。”

Omid Rezania,CalPERS 基金

您也可以从以下列表中选择网站:

美洲

- América Latina (Español)

- Canada (English)

- United States (English)

欧洲

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)

亚太

- Australia (English)

- India (English)

- New Zealand (English)

- 中国

- 日本Japanese (日本語)

- 한국Korean (한국어)