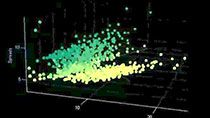

Standard & Poor’s makes extensive use of quantitative models in many ways, including analyzing market conditions, forecasting stress scenarios, supporting credit analysis, and evaluating pricing for complex debt instruments. One important aspect of ensuring model quality is rigorous ongoing validation, particularly for models that are recalibrated daily.

This presentation provides an overview of a framework deployed at S&P that incorporates MATLAB to produce and analyze daily validation reports. The credit default swap–based Market Derived Signals model is introduced briefly, and the corresponding automated framework for daily validation of model output is discussed. Additional reports that allow for time series analysis of model behavior over a specified time period are also considered.

We briefly describe a dashboard currently under development that automatically evaluates the validation output and provides a compact display of the information. Finally, we provide an overview of the technical infrastructure that was built to support the engine that drives the validation framework.